Deciding to invest in hospitality is not the hard part. The hard part is choosing where within the sector your capital belongs. Hotels get most of the attention, the analyst coverage, and the institutional capital. Hostels, by contrast, remain remarkably under-researched — and for contrarian investors, that is exactly where opportunity lives.

Definition: Investing in hospitality means committing capital to businesses in the accommodation, catering or travel-related sectors — hotels, resorts, hostels, serviced apartments, restaurants — with the aim of generating income and capital appreciation from tourist demand.

Within this broad category, the hostel sub-sector has consistently delivered higher RevPAR returns, lower entry costs and greater occupancy stability than traditional hotels.

The global hotel sector is forecast to reach €79.6 billion in investment volume by 2026; however, the hostel sub-sector remains undercapitalised relative to its growth rate. The global hostel market was valued at €5.185–5.44 billion in 2026 and is projected to reach €8.321–13.175 billion between 2030 and 2036, with a CAGR of 6.5–11.6% according to sources.

For investors willing to go where institutional money has not yet fully arrived, now is the right time to act.

This guide answers all the key questions that investors researching the hospitality sector ask themselves: what does ‘investing in hospitality’ mean, why does the hospitality sector outperform others, how to enter at different capital levels, which metrics matter, where the risks lie, and how to get started step by step. If you’re considering investing in hospitality in 2026, this is the go-to guide you need.

What does it mean to invest in hospitality?

When investors consider entering the hospitality sector, they typically mean one of three things: buying equity in publicly traded hotel companies or REITs, committing capital to a private real estate vehicle that owns accommodation assets, or directly acquiring and operating a property. All three paths exist within the hostel sub-segment and each carries a distinct risk-return profile.

Scope of the hospitality sector

The hospitality sector is far broader than hotels alone. It includes full-service and select-service hotels, luxury resorts, boutique properties, serviced apartments, extended-stay facilities, hostels, restaurants, bars, casinos, and the technology platforms that support all of the above. For most investors, the decision to allocate capital within hospitality narrows to accommodation assets — and within accommodation, the choice between traditional hotels and the growing hostel sub-segment is increasingly decisive.

Hostel assets differ from hotel assets in several fundamental ways that make them structurally attractive:

- Revenue density: A 4-bed dorm generates more revenue per square metre than a standard hotel double room, even at a fraction of the per-night rate.

- Lower entry cost: A hostel renovation project typically requires €300,000–€500,000; an equivalent boutique hotel acquisition starts at €2–5 million in the same European city.

- Demand durability: Budget accommodation demand is more resilient to economic cycles — when consumers tighten spending, they downgrade from hotels to hostels, not away from travel entirely.

- Higher margin ancillary revenue: Food and beverage operations in hostels carry 65% profit margins (HVS data), and bar, events, and tour income add meaningful yield above room revenue.

Hostel vs. Hotel: The investment case at a glance

| Dimension | Traditional Hotel | Hostel | Advantage |

|---|---|---|---|

| Entry cost (European city) | €2M–10M+ | €300K–1.5M | Hostel ✓ |

| Typical annual yield | 5–6% | 6–8% | Hostel ✓ |

| Avg. occupancy (urban) | 63–72% | 80–86% | Hostel ✓ |

| Revenue density (per m²) | Standard | Higher (multi-bed) | Hostel ✓ |

| F&B margin | 30–38% | Up to 65% | Hostel ✓ |

| Market growth (CAGR) | ~5–7% (select) | 6.5–11.6% | Hostel ✓ |

| Institutional competition | Very high | Moderate | Hostel ✓ |

| Operational complexity | High | High | Equal |

| Liquidity (direct) | Low | Low | Equal |

Sources: Christie & Co, HVS, Tranio, Grand View Research. Yields are indicative; actual returns depend on location, management, and leverage.

Why invest in hospitality through hostels in 2026?

The fundamental case for the hostel sub-sector within hospitality rests on three pillars: structural demand growth, competitive yield advantage over traditional hotels, and a market consolidation wave that is creating exceptional entry windows for well-positioned investors right now.

€5,4B

Global hostel market 2026

11.6%

CAGR 2025–26 (Business Research Co.)

86%

Avg. occupancy, Onefam chain Europe

€776M

Brookfield deal for Generator portfolio

Structural demand drivers

Anyone who studies travel demographics before entering the hospitality sector quickly identifies the same three forces driving hostel demand upward: the continued growth of Millennial and Gen Z travel, the rise of solo and experiential travel, and the structural expansion of digital nomadism.

- Youth travel volume: More than 58% of young travelers globally now prefer hostels as their primary accommodation category. The Millennial and Gen Z cohort that drives this demand is currently the largest travel-spending demographic on earth.

- Solo travel: The backpackers and solo travelers segment holds 55.53% of global hostel market revenue. Solo travel is growing faster than group or family travel across every major origin market.

- Digital nomadism: The demand for extended-stay, coworking-integrated hostel accommodation is generating a new revenue stream that traditional hotels are poorly equipped to serve. Hostels are naturally positioned for this shift — communal kitchens, lounge areas, and social programming already align with what digital nomads need.

- Experiential travel: The shift from “buy things” to “do things” is a multi-decade consumer megatrend that directly benefits hostels. Guests are willing to pay for curated experiences — city walks, cooking classes, social events — not just a bed.

The consolidation wave: Why right now matters

For investors seeking timing advantage in hospitality, 2025–2026 marks a significant inflection point in the hostel sector. Institutional capital has arrived, valuations are rising, but the market remains fragmented enough that well-positioned mid-market buyers can still acquire assets before full institutionalisation compresses yields.

The deal flow tells the story clearly:

- Brookfield asset management acquired Generator Hostels’ European portfolio for €776 million in May 2025 — the single largest hostel deal in history, signalling that €100B+ institutions now view hostels as core hospitality assets.

- Room00 (formerly TOC Hostels + Room00) announced plans to invest €330–420 million in 2026 to add 20 properties across Spain, Italy, Portugal, and the UK, backed by a €400 million funding round led by Kings Street.

- Invel Real Estate formed a €200 million partnership with YellowSquare in early 2025 to expand hybrid hospitality across Southern Europe.

“A lot of capital is looking to build a strong footprint in the sector, which will create some consolidation down the road.”

— Hospitality Investor, January 2026

Consolidation compresses entry yields for late arrivals but dramatically increases exit liquidity for early movers. Investors who enter the hospitality sector now through hostel assets in prime European cities are buying ahead of the yield compression that institutional consolidation invariably produces.

The yield advantage: Numbers that matter

Christie & Co data shows that hostel returns typically run 6–7% annually in European cities — consistently above the 5–6% equivalent hotels generate in the same locations. That differential may sound modest in isolation, but compounded over a 7–10 year hold period it represents meaningful outperformance.

The most striking evidence comes from direct ownership cases. Howzit Hostels, North America’s top-rated small hostel, purchased a building for €697.850 and budgeted €680.000 in NOI for 2025 — a near 1:1 return on original purchase price achieved in approximately five years. The co-founder’s stated target for their portfolio: returns north of 20% IRRs and 2.5 to 3 multipliers over a seven-year hold period.

How to Invest in Hospitality: Every vehicle explained

There is no single right way to enter the hostel segment when allocating capital to hospitality. The appropriate vehicle depends on available capital, desired involvement level, liquidity requirements, and risk tolerance. The following covers every viable entry point, from the smallest passive position to full direct ownership.

| Vehicle | Min. Capital | Liquidity | Target Return | Involvement | Risk |

|---|---|---|---|---|---|

| Hotel/Hospitality REITs & ETFs | ~€100 | Daily | 4–8% total | Passive | Medium |

| Hospitality Stocks (Accor, IHG…) | ~€50 | Daily | Market-driven | Passive | High |

| Crowdfunding (hostel projects) | €1K–€25K | Illiquid (3–7 yr) | 8–14% IRR | Passive | Medium |

| ★ Hostel Chain Revenue-Share | €50K–€100K | Illiquid (5 yr) | 18–24% IRR | Fully passive | Medium |

| ★ Hostel Chain Investment (JV) | €200K–€2M | Illiquid (5–10 yr) | 15–20% IRR | Passive/semi | Medium |

| ★ Direct Hostel Ownership | €300K–€1.5M | Very illiquid | 6–8% yield; 20%+ IRR value-add | Active | High |

REITs and ETFs: Liquid hospitality exposure

For investors seeking liquid hospitality exposure without committing illiquid capital, publicly traded hotel REITs and broad REIT ETFs (such as VNQ or IYR) offer daily liquidity and dividend income. While few listed vehicles are pure-play hostel REITs, major operators with hostel exposure — such as Accor (with its Jo&Joe brand) — are accessible through public markets.

Historical dividend yields for hospitality REITs range from 4–8%, with total returns (dividends plus price appreciation) varying significantly by cycle timing.

One of the most compelling ways to gain hostel exposure without operational involvement is the revenue-share model offered by growing hostel chains. Under this structure — exemplified by The Hosteller in India — investors fund the transformation of a leased property (approximately €60,000 for a 20-room hostel) and receive a monthly percentage of revenue for a 5-year term.

The Hosteller reports 18–24% IRR across 30 active properties with monthly payouts. This is fully passive investing in hospitality with direct hostel exposure.

Chain Investment and joint ventures

Onefam Hostels — the most awarded hostel brand in Europe across 2024–2025–2026 — actively seeks investment partners for new property expansion across Barcelona, Madrid, London, Amsterdam, Prague, Budapest, Porto, Seville, Rome, and Florence.

Their model achieves an 86% average occupancy rate across 19 hostels in 8 cities, built on centralized revenue management, brand-driven demand, and economies of scale. Investing in an established chain rather than a single asset reduces risk through diversification while maintaining the yield premium of the hostel model.

Direct Hostel ownership

Direct acquisition is the highest-conviction, highest-involvement way to invest in hospitality through hostels. It requires the most capital (€300,000–€500,000 minimum for a renovation project, €1–1.5 million for an operating business) and the deepest operational expertise.

In return, it offers the greatest control over value creation — through repositioning, brand improvement, ancillary revenue development, and eventual exit to institutional buyers. A well-located, well-operated hostel in a European tourism hub can achieve annual yields of 6–8% from day one, with value-add upside substantially higher.

A 100-bed hostel in Barcelona’s Eixample district, acquired for €1.1 million with 78% occupancy and an average bed rate of €22, generates approximately €625,000 in annual room revenue. Apply a 35% GOP margin plus €90,000 in F&B profit, and NOI reaches approximately €309,000 — a 28% yield on equity assuming 50% leverage.

Practical Example

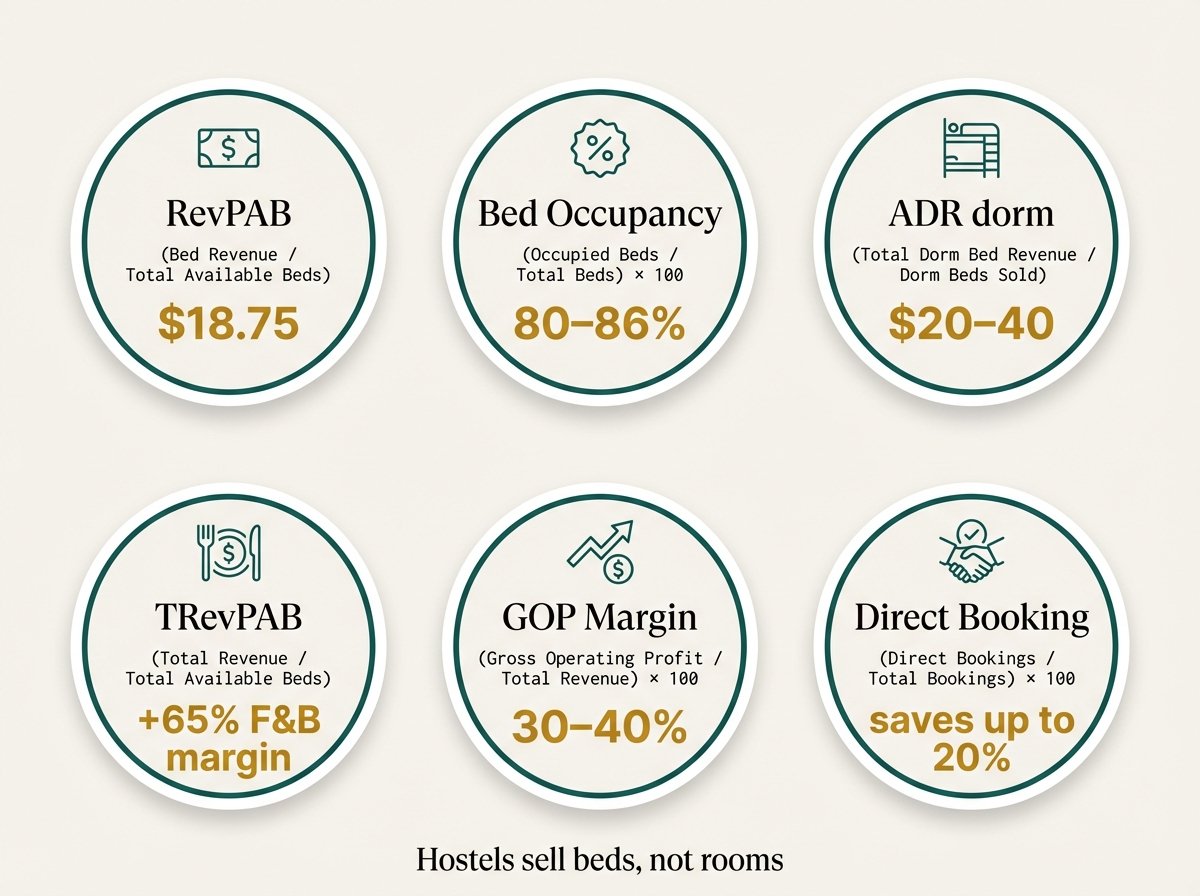

Key Metrics for Investors: The Hostel KPI toolkit

Investors evaluating hostel assets need a different set of KPIs than those evaluating traditional hotels. The primary difference: hostels sell beds, not rooms. This shifts the performance measurement framework in important ways.

| KPI | Formula | Description for Investors |

|---|---|---|

| RevPAB | Room Revenue ÷ Available Beds | Revenue Per Available Bed — the hostel industry’s equivalent of the hotel industry’s RevPAR. A hostel with 75% occupancy and an ADR of €21 generates €16 RevPAB. A key underwriting metric when deciding to invest in the hospitality sector through hostel assets. |

| Bed Occupancy | Beds Sold ÷ Beds Available | Bed occupancy rate. Well-managed city hostels typically achieve 80–90%. Onefam averages 86%. A 5% increase in a 100-bed hostel with an ADR of €30 generates an additional €54,294 per year. |

| ADR (per bed) | Room Revenue ÷ Beds Sold | Average Daily Rate per bed. This should be calculated separately for dormitories (€17–€34) and private rooms (€55–€81). Dynamic pricing across segments is a key driver of value creation. |

| TRevPAB | Total Revenue ÷ Available Beds | Total Revenue Per Available Bed. The most comprehensive metric: It includes revenue per room plus F&B, tours, events, ticket sales, and ancillary services. F&B at hostels can reach a gross margin of up to 65% (HVS). |

| GOP Margin | (Revenue − Op. Costs) ÷ Revenue | Gross Operating Profit Margin. Well-managed hotel operations aim for margins of 30–40%. This is achievable with high occupancy, a high rate of direct bookings, and well-developed ancillary revenue streams. |

| Direct Booking % | Direct ÷ Total Bookings | Direct booking percentage. Every percentage point shifted away from OTAs saves 10–20% in commission. A hostel with €600,000 in revenue saves €60,000–€120,000 a year by moving from 0% to 100% direct bookings. |

Risks when you invest in hospitality through Hostels

Every investor in the hospitality sector must engage seriously with risk. Hostels offer superior yields and growth rates versus traditional hotels — but they carry their own specific risk profile that demands attention before capital is committed.

| Risk | Level | Description |

|---|---|---|

| Operational intensity | 🔴 High | Hostels require specialized, round-the-clock management. Profitability is highly dependent on the quality of the operator. An unsuitable operator can turn a 30% gross operating profit margin into a loss. |

| Location-dependent | 🔴 High | A hostel in a city without an established backpacker scene, tourist attractions, or a digital nomad community will perform significantly worse. Location accounts for 80% of the underwriting decision. |

| Regulatory risk | 🟡 Medium | Restrictions on short-term rentals in cities such as Barcelona and Amsterdam may affect hospitality licenses. Regulations vary by city and change frequently. Be sure to check before purchasing. |

| Pressure from OTA commissions | 🟡 Medium | Hostelworld, Booking.com y Airbnb cobran comisiones del 10–20%. Las propiedades sin reconocimiento de marca ni capacidad de reserva directa ceden márgenes significativos a las plataformas de distribución. |

| Alternative competition | 🟡 Medium | Budget hotel chains (OYO, ibis Budget) and Airbnb shared rooms are in direct competition with hostels. Differentiating through design, experience, and community programming is essential. |

| Demand Cyclicality | 🟢 Low | Lower than that of traditional hotels. Demand for budget accommodations is more recession-resistant—consumers opt for hostels instead of canceling their trips. This countercyclical characteristic provides greater stability than luxury hotels. |

Risk Mitigation Framework: Investors who achieve success in the hospitality industry through hostels consistently do three things: they invest in cities with a proven, diversified tourism market; they partner with experienced operators rather than managing properties in-house; and they develop properties with unique offerings—such as bars, events, and coworking spaces—that build customer loyalty and reduce dependence on OTAs. These three measures simultaneously address the three highest-risk factors.

Where to Invest in Hospitality: Best Hostel Markets in 2026

Geography is the most important variable in hostel investment underwriting. Investors targeting hostel assets must prioritise cities with high, diversified, year-round tourism demand, a proven backpacker and young traveller circuit, and a regulatory environment that supports commercial hostel operations.

Europe: The dominant market

Europe holds 35.4% of the global hostel market (approximately €2,05 billion in 2025) and remains the single best geographic concentration for investors looking to deploy hospitality capital at scale. The region’s dominance rests on dense inter-city rail networks, entrenched youth travel culture, and mature hostel infrastructure in key gateway cities.

Top European Hostel cities for investment in 2026

Based on transaction volume, occupancy data, chain expansion priorities, and institutional deal flow:

- Barcelona & Madrid: Spain reached €2.9B in total hospitality deal volume through Q3 2025 (+40% YoY). Room00 and Onefam are both expanding aggressively. Prime hostel beds trade above €80,000/bed.

- Lisbon & Porto: Among Europe’s fastest-growing backpacker circuits. Rising ADR, stable occupancy, and lower entry prices than Iberian competitors.

- Rome & Florence: Room00’s Italian allocation of €120–140M in 2026 signals institutional conviction. Entry opportunities remain ahead of full market maturation.

- London: Room00 targeting 5 new properties in Bloomsbury, Paddington, St Paul’s, and Victoria. High ADR potential; strong student and backpacker demand year-round.

- Prague & Budapest: Central European cities with very high backpacker volume, low operating costs, and established hostel ecosystems — ideal for first-time investors in hospitality.

- Amsterdam: High demand, strong institutional interest, regulatory constraints require careful licensing due diligence before acquisition.

Asia-Pacific: Fastest-growing market

Asia-Pacific is the fastest-growing regional hostel market, projected to expand at approximately 9.3% CAGR through 2034. Investors with a growth-first mandate should examine this region carefully. India’s hostel market is growing at double-digit rates, driven by a youth population exceeding 600 million and rapidly expanding domestic tourism.

Japan — driven by record inbound arrivals of 38.7 million in 2025 and a weakened yen — offers premium hostel ADR potential in Tokyo, Osaka, and Kyoto. Thailand’s backpacker circuit (Bangkok, Chiang Mai, Bali, islands) sustains robust year-round occupancy.

North America: Niche but high-ADR

The North American hostel market is growing at 5.3–6.1% CAGR and reached €1,25 billion in 2024. While institutional penetration is lower than Europe, it creates opportunity. Approximately 49% of American Millennials prefer shared-stay formats, yet the US hostel supply per capita is a fraction of European levels.

The Howzit Hostels case — Hawaii-based, €698K purchase, €680K 2025 NOI budget — demonstrates that investors who invest in hospitality through US hostels in the right location can achieve exceptional returns precisely because the competitive supply is so thin.

How to evaluate a Hostel Investment: Due diligence checklist

The due diligence process for hostel assets differs materially from standard hotel or residential property analysis. You are evaluating an operating business as much as a real estate asset. The following checklist covers every dimension that serious investors must address.

- Location footfall: Confirm the city and neighbourhood have a proven, year-round backpacker and young traveller circuit — not just summer tourism peaks. Check Hostelworld search volume data for the specific destination.

- Bed occupancy history: Verify at least 2–3 years of monthly bed occupancy data, separating dorm vs. private rooms. Target above 75% annually; 80%+ is strong.

- RevPAB and TRevPAB: Model forward revenue projections based on RevPAB data — not just room revenue. Include bar, tours, events, and locker income.

- Direct booking ratio: A high OTA dependency (>60% of bookings through platforms) suppresses margin and signals weak brand equity. Upside exists if you can shift mix.

- GOP margin and cost structure: Review at least 24 months of P&L. Labour cost should be 25–35% of revenue in a well-run operation. Higher signals staffing inefficiency.

- Licensing and regulatory status: Confirm the hostel holds all required municipal licences for commercial accommodation. In cities with active short-term rental regulation, verify the licence is transferable on acquisition.

- Physical condition and CapEx: Commission a property condition assessment. Budget a replacement reserve of 3–5% of annual revenue for ongoing CapEx — bunk beds, common area furniture, bathrooms, and technology systems require continuous reinvestment.

- Operator quality: If acquiring with an existing management team, review Hostelworld ratings (target 8.5+), Google reviews, and staff turnover. Management quality is the single largest predictor of hostel NOI performance.

- Brand affiliation: A hostel affiliated with a recognized chain (Generator, Selina, A&O, Onefam) generates 15–25% more bookings at higher ADR than comparable independents in the same market.

- Exit market depth: Map the buyer universe for the asset at exit. Institutional buyers (Brookfield, Invel, Room00) are increasingly active but remain focused on scale — single small assets are best exited to local operators or private family offices.

⚠️ ⚠️ Common underwriting mistakes: Overestimating occupancy in the first year. Repositioning projects should be modelled at 60–65% in year one and 75–80% in year three. Assuming immediate occupancy of 85%+ is the most common mistake.

Ignoring OTA commissions in the profit and loss account. With an average commission of 15% on 70% of bookings, a hostel with €600K in revenue pays €63,000 a year to the platforms — a figure that must be explicitly included in all return projections.

How to Invest in Hospitality Through Hostels: Step by Step

Whether you have €50,000 or €5 million available, the process follows the same logical sequence. The steps below apply universally; only the vehicle and scale change.

- Define your objectives and capital clearly. Determine whether you are targeting passive income (revenue-share, REIT), capital appreciation (value-add direct acquisition), or both. Establish your time horizon (5 years vs. 10 years) and your liquidity requirements. Direct hostel investing is illiquid — your capital will be committed for the life of the deal.

- Choose the right vehicle for your capital tier. Under €100K: revenue-share programs with established hostel chains (The Hosteller model, 18–24% IRR) or crowdfunding platforms with hostel project exposure. €100K–€500K: hostel chain JV partnerships or co-investment in multi-property platforms (Onefam, Room00). €500K+: direct acquisition of an operating hostel or development of a hostel conversion project.

- Select your target markets. Prioritise cities with proven backpacker circuits, limited hostel supply relative to demand, and favourable regulatory environments. For European investors, Spain, Portugal, and Italy offer the best combination of yield, growth, and deal flow in 2026. For Asia-Pacific exposure, India and Thailand offer high-growth entry windows.

- Build your team before you commit capital. You need: a hospitality-focused legal advisor who understands hostel licensing in your target market; an accountant familiar with operational real estate; and an experienced hostel operator or asset manager. Do not pursue a direct hostel acquisition without a qualified operator structure in place from day one.

- Execute thorough financial due diligence. Use the checklist above. Build three scenarios in your financial model: base case (75% occupancy, current ADR), downside (60% occupancy, ADR −10%), and upside (85% occupancy, ADR +15% through repositioning). Only proceed if the downside scenario still services debt and preserves capital.

- Structure for tax efficiency from day one. Hostel assets held through appropriate vehicles (LLCs, LPs, offshore structures depending on jurisdiction) can benefit materially from accelerated depreciation, operational loss offsets, and pass-through income structures. Securing proper tax advice before acquisition prevents costly restructuring later.

💡 Where to start right now: If you’re new to investing in hospitality and are drawn to the sector, start with a €50,000–€100,000 investment in a revenue-share programme with an established chain.

This gives you real exposure to the hospitality economy — occupancy patterns, RevPAR cycles, F&B margin dynamics — whilst building the market knowledge needed to underwrite a direct acquisition. The sector rewards investors who understand its operational fundamentals before committing seven-figure sums.

Frequently Asked Questions: Invest in Hospitality

Is investing in hospitality a good idea in 2026?

Yes — and the hostel sub-sector offers the most compelling entry point within hospitality right now. The global hostel market is growing at 6.5–11.6% CAGR, yields consistently exceed equivalent hotels by 1–2 percentage points, and the consolidation wave (Brookfield, Room00, Invel) is driving exit liquidity for early-stage positions. Investors who invest in hospitality through hostels today are entering ahead of full institutional pricing. The key caveat: location and management quality are non-negotiable. A poorly located or poorly managed hostel will underperform even a mediocre hotel.

How much capital do I need to invest in hospitality?

The required capital depends on the vehicle. Revenue-share programs with hostel chains allow you to invest in hospitality from approximately €50.000–€100.000. Crowdfunding platforms with hostel exposure start from €1.000–€25.000.

A hostel renovation or conversion project requires €300,000–€500,000 minimum. An established operating hostel in a European city costs €1–1.5 million. Institutional-scale chain investments start at €10 million and above. For most retail investors, the revenue-share and chain investment models are the most accessible and risk-appropriate starting points.

What returns can I realistically expect when I invest in hospitality through hostels?

Stable hostel operations in prime European cities deliver 6–8% annual yields — 1–2 percentage points above equivalent hotels. Revenue-share programs report 18–24% IRR targets. Value-add direct acquisitions (buy underperforming, reposition, optimise) target 20%+ IRR over 7-year holds.

The Howzit Hostels case (€698K building, €680K 2025 NOI budget) represents the extreme upside of value-add hostel investing. Realistic base-case targets for investors who invest in hospitality through well-located hostel assets: 8–12% cash-on-cash yield by year three, 15–20% IRR at exit.

What is RevPAB and why is it essential to understand before I invest in hospitality?

RevPAB (Revenue Per Available Bed) is to hostel investing what RevPAR is to hotel investing — the primary performance indicator. It equals total room revenue divided by total available beds, regardless of occupancy. A hostel with 100 beds at 75% occupancy and €21 ADR generates a RevPAB of €16.

Understanding RevPAB allows you to compare hostel performance across different property sizes and markets. It is the single most important metric to model when you invest in hospitality through a hostel asset, because it captures both pricing power and occupancy efficiency in one number.

Hostel vs. hotel: where should I invest in hospitality?

For most investors entering the sector for the first time, hostels offer a more compelling combination of lower entry cost, higher growth rate, superior yield, and stronger occupancy resilience than traditional hotels. Christie & Co data consistently shows hostel yields 1–2 points above hotel yields in the same European cities.

The hospitality sector is bifurcating: luxury hotels are capturing institutional capital at compressed yields; mid-market hotels face genuine operational headwinds; budget accommodation — including hostels — benefits from counter-cyclical demand and the structural growth of youth, solo, and nomadic travel.

What are the best cities to invest in hospitality through hostels?

In Europe, Barcelona, Madrid, Lisbon, Porto, Rome, Florence, London, Prague, and Budapest offer the strongest combination of demand depth, yield, and deal flow. Room00’s 2026 Italian expansion (€120–140M) and its London entry (€50–80M) signal institutional conviction in these geographies.

In Asia-Pacific, Tokyo, Bangkok, and India’s major cities offer high-growth early-mover windows. In North America, Hawaii and New York represent niche high-ADR opportunities. The best cities to invest in hospitality through hostels are those with diversified tourism demand — not single-event or single-season dependent markets.

The verdict: The best place to invest in Hospitality in 2026

When you map every dimension of the decision — yield, growth rate, entry cost, occupancy resilience, demand demographics, and the institutional deal flow signalling where smart money is moving — the hostel sub-sector emerges as the most compelling place to invest in hospitality in 2026.

Traditional hotels offer familiarity and scale. Luxury hotels offer prestige and strong near-term performance in gateway cities.

But for investors who want to invest in hospitality with a genuine risk-adjusted return advantage, hostels deliver structurally higher yields, lower entry capital requirements, more resilient occupancy patterns, and a demand growth story tied to the fastest-expanding travel demographic on earth.

The consolidation wave — Brookfield’s €776 million Generator acquisition, Room00’s €330–420 million 2026 expansion, Invel’s €200 million YellowSquare partnership — confirms that the smartest institutional capital has already arrived at this conclusion.

The window to invest in hospitality through hostel assets ahead of full yield compression is open, but it will not stay open indefinitely.

The investors who will look back on 2026 as the defining entry point are those who did three things: chose a city with proven, diversified tourism demand; committed to experienced hostel operators rather than managing in-house; and understood RevPAB, TRevPAB, and direct booking economics well enough to underwrite confidently.

Every decision to invest in hospitality should begin with exactly this kind of evidence-based framework. This guide has equipped you with all three.

Sources and data references

- Brookfield’s Acquisition of Generator Hostels (€776 million)

- Room00 Expansion / €330–420 million in 2026

- Howzit Hostels Case

- Yields hostels 6–7% vs hoteles 5–6% (Christie & Co)

- Global hostel market size

Disclaimer: This article is for informational purposes only and does not constitute investment, legal, or financial advice. All investments involve risk. Past performance is not indicative of future results. Please consult a qualified financial adviser before making any investment decision.